Introduction: Tight supply and high prices of raw material octanol have put significant cost pressure on DOTP producers. Coupled with the New Year's Day holiday, DOTP plant operating rates have dropped significantly. On January 2nd, DOTP plant operating rates fell to 48%, a 17% decrease from December 22nd (10 days prior), with daily output falling by nearly 1600 tons. As of today, operating rates have slightly recovered, currently around 53%, but remain at a low level for the year.

I. Raw material octanol is in short supply and at a high price.

Isooctyl Alcohol production in December reached 276,500 tons, an increase of 28,700 tons from November, representing a month-on-month increase of 11.58%. The Shandong Dongming Oriental plant restarted operations; however, due to the unstable operation of octanol plants in Zhejiang and some other regions, the market still experienced significant supply losses, and the overall domestic supply failed to meet expectations. On the demand side, domestic octanol consumption in December was 291,800 tons, a decrease of 16,800 tons from November. Even with the decline in demand, octanol supply remained lower than demand in December, resulting in a supply-demand gap of 13,300 tons. This tight supply-demand situation supported continued high-level price fluctuations in the octanol market .

Table of Isooctyl Alcohol supply and demand balance in December

Indicator Name | November | December |

Yield | 24.78 | 27.65 |

Import volume | 1.21 | 1.2 |

Downstream consumption | 30.86 | 29.18 |

Export volume | 0.98 | 1 |

supply and demand gap | -5.85 | -1.33 |

After the Jiangsu Huachang new plant and the Shandong Jianlan plant completed their commissioning, the load increase process was relatively slow. Furthermore, the Jiangsu Huachang new plant entered a shutdown maintenance phase at the end of the month, resulting in a very limited contribution from both plants to the monthly supply. Against this backdrop, the domestic octanol market supply failed to increase as expected, and domestic supply remained tight.

After prices rose to a high level in mid-month, downstream resistance gradually emerged. Coupled with the impact of expectations for new plant commissioning, market prices came under downward pressure in the high-price range. However, supported by the slow increase in the operating rate of new plants, low-price offers in the market showed strong resilience. In addition, downstream users' raw material inventories have been at low levels for a long time, and at the end of the month, two plants in East China experienced sudden operational fluctuations, affecting the operation of some downstream plants. These multiple factors combined to drive the octanol market to rebound again.

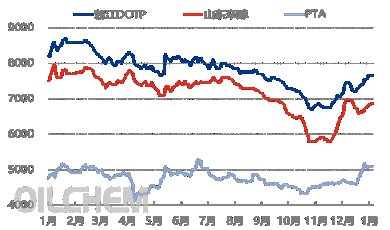

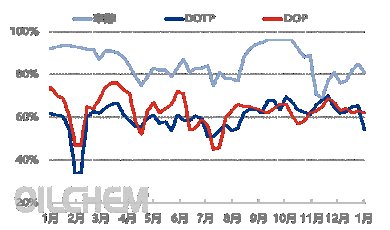

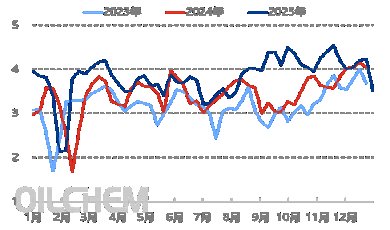

Figure 1. Price trend of DOTP and raw materials in 2025 (RMB/ton) | Figure 2. Weekly operating rate trend of octanol and downstream products |

|  |

|

|

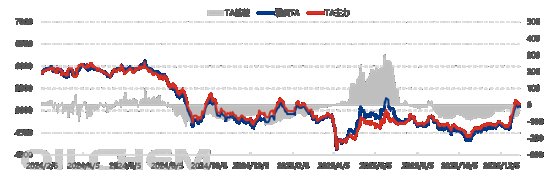

II. PTA prices fluctuated at high levels.

Figure 3. PTA spot basis trend (RMB/ton) |

|

|

Since late December, the PTA market has shown a positive trend with both absolute prices and spot basis rising. Firstly, the strong rebound in crude oil prices from their recent lows has not only directly boosted the cost support for PTA but also improved trading sentiment across the entire commodity market. Secondly, the market has strong expectations for structural improvements in upstream PX products, leading to high investor sentiment and further strengthening the cost transmission logic of PTA. Thirdly, the structural contradiction between PTA and downstream PET has eased significantly, postponing inventory pressure in the industry. Coupled with unplanned production cuts by several PTA plants during the month, market supply has tightened. These multiple positive factors have combined to drive the PTA market price upward. Currently, the reference price for PTA in East China is 5097 yuan/ton, an increase of 503 yuan/ton from the monthly low of 4594 yuan/ton on December 16th, representing a rise of 10.95%.

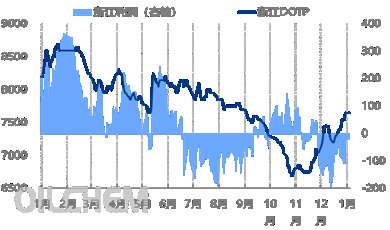

III. Cost pressures coupled with the New Year's Day holiday led to a significant decline in DOTP (Doctoral Research Institute) operations.

Despite cost support keeping DOTP prices relatively strong, end-user demand was limited around the New Year's Day holiday , resulting in lackluster new order performance and a lack of sustained volume growth. Faced with high DOTP raw material prices, downstream users adopted a cautious purchasing attitude, hindering the transmission of DOTP prices to downstream users and continuously squeezing industry profit margins. Most companies remain operating at a loss. Taking Zhejiang province as an example, the theoretical average loss for DOTP among sample companies remained at 61 yuan/ton this week, continuing within the loss-making range throughout the week, and no significant signs of improvement have been observed so far.

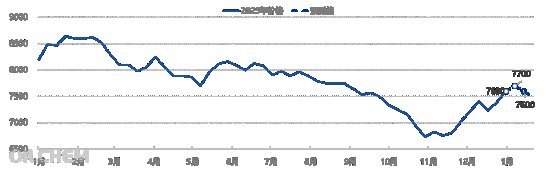

Figure 4. Price and Profit Trends of DOTP in 2025 (RMB/ton) | Figure 5. Comparison of Weekly DOTP Production Trends (10,000 tons) from 2023 to 2025 |

|

|

Due to cost pressures and the New Year's Day holiday, DOTP manufacturers were not very active in production, with operating rates significantly lower than last week. Specifically, Guangzhou Weilianda and Huangshan Hanghua, which shut down around New Year's Day, have now restarted; Fujian Chunda remains shut down; Shandong Langhui's plant reduced production; and Ningbo Nanya, after a brief restart, shut down again today due to unexpected fluctuations in its equipment. According to Longzhong Information, China's DOTP production this week was 35,100 tons, a decrease of 7,200 tons, or 17%, compared to last week; the weekly average capacity utilization rate was 54.17%, a decrease of 11.31 percentage points from last week.

IV. Market Outlook

Figure 6. Changes in the DOTP main market price over the next three weeks (RMB/ton) |

Strong cost support is the core driver of the market trend. The tight supply of octanol, a key raw material, remains unchanged, keeping prices high. PTA, another important raw material, is also expected to maintain its strong price trend, driven by continued cost support and a still tight supply-demand market structure. This dual support from high raw material prices has created a solid bottom for DOTP prices. There are also positive factors supporting the supply side. It is expected that the operating rate of DOTP plants will remain low next week, and the tight supply situation in some regions will be difficult to alleviate effectively. The support from the supply side will further consolidate the market's sentiment to maintain prices. However, weak demand will continue to constrain market prices. The lack of substantial positive factors for downstream end-users means that buyers may remain cautious about following up on high-priced goods, which will limit the upside potential of DOTP prices. In summary, the current DOTP market is supported by both cost and supply factors, but the weakness on the demand side will limit the pace of price increases. It is expected that the DOTP market price will continue to operate firmly in the short term, with the ex-factory price of DOTP fluctuating between 7,600-7,800 yuan/ton, showing an overall pattern of firm operation and limited price increases.

|

|