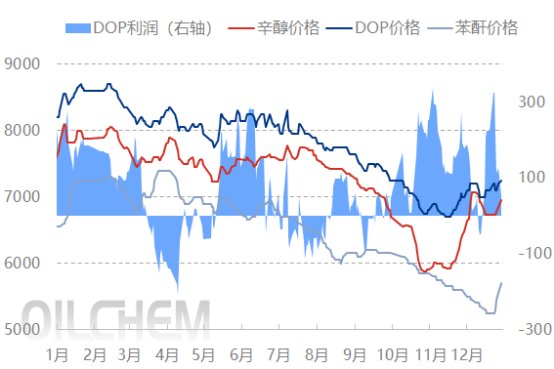

Introduction: With the prices of raw materials surging, the cost of DOP has increased by more than 5% recently, driving up DOP prices . However, the high cost has led to a decrease in profitability of more than 50%.

Local spot market tightness drives up DOP prices

Starting in November, news of production cuts and shutdowns of octanol continued to emerge, leading to a decrease in market supply. Due to factors such as insufficient DOP octanol or unexpected production stoppages, production decreased to varying degrees, causing the market supply to decline. By the end of December, spot supply in East China was tight, and many suppliers began to queue up for delivery.

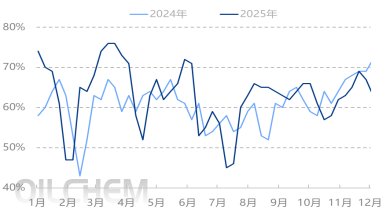

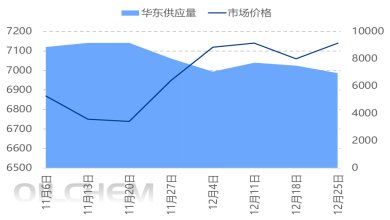

Figure 1. Weekly capacity utilization rate trend of DOP from 2024 to 2025 (%) | Figure 2. Changes in DOP supply and price in East China, November-December 2025 (tons, yuan/ton) |

|

|

|

|

During November and December, multiple plants in East China experienced varying periods of reduced or halted production. Weekly supply peaked in early November at 9,170 tons, but by the end of December, weekly output had fallen to less than 7,000 tons, a 24% decrease from the peak. Meanwhile, the octanol market was tight, and DOP prices continued to rise. As of December 31, the price in Jiangsu was 7,350 yuan/ton, an increase of 450 yuan/ton from the beginning of November, or 6.52%. With end-users replenishing their stocks and traders making up for short positions, the supply shortage in East China intensified, leading to varying degrees of delivery delays.

DOP costs remain high while profits decline.

Since November, the price of octanol has been fluctuating upwards. By the end of December, the price of octanol in Shandong reached 6,825 yuan/ton, an increase of 975 yuan/ton or 16.67% compared to the beginning of November. Meanwhile, the market for another raw material, phthalic anhydride, continued to decline. By mid-December, the price of phthalic anhydride had fallen to a low of 5,250 yuan/ton for the year, offsetting some of the cost pressure brought by the rise in octanol. By mid-December, the cost price of DOP in the market had increased by 279 yuan/ton, an increase of 4.38% compared to the beginning of November. During this period, the profit of DOP in the market remained in the range of 200-300 yuan/ton for most of the time.

Due to a planned production cut in o-phthalic anhydride in January, prices began to rise at the end of December. Phthalic anhydride prices had already absorbed the impact of rising raw material prices, resulting in a strong rebound. In East China, the weekly increase in o-phthalic anhydride reached 600 yuan/ton to 5900 yuan/ton, reaching a two-month high. Coupled with the increase in octanol prices, the weekly increase in DOP cost was 400 yuan/ton, but the price increase only followed by 250 yuan/ton. As a result, the profit level dropped to 50-100 yuan/ton, with a significant decrease in profits.

DOP trading at high levels will be limited, leading to significant supply and demand pressure next month.

From the perspective of the raw material market, the tight spot market for octanol is supporting high prices. Currently, most industry players are taking a wait-and-see approach, waiting for the plant recovery progress after the short holiday. Meanwhile, the price of phthalic anhydride has risen too quickly, and buying interest at high levels has begun to weaken. DOP traders are mostly taking a wait-and-see attitude regarding the trend of raw material prices after the holiday.

From the perspective of supply and demand, after prices have remained high, the boost to end-user demand has been limited, and the willingness to purchase high-priced goods has weakened. New orders have decreased, and with the plants operating normally during the New Year's Day holiday, the backlog of deliveries in East China is expected to ease after the holiday.

The DOP market has seen slow follow-up in high-priced transactions, and the market is still mainly driven by raw materials. In January, most DOP plants maintained normal operation, with only Li & Fung's 50,000-ton-per-year plant clearly shutting down. From the New Year's Day to the Lunar New Year period, there is little effective sales time in February, and the latter half of January will be used to take on some of the sales tasks for February's goods. Overall, the supply and demand pressure in January is relatively high, and end-users' purchasing and stocking will still depend on price performance. It is expected that the DOP market may open high and then fall next month, with the middle and latter parts of the month still focusing on shipments.