Introduction: Since December, the DOTP industry has been mired in persistent losses, with most companies operating under pressure. Taking the Zhejiang market as an example, as of now, the average monthly theoretical profit of sample companies is -119 yuan/ton, a significant drop of 124 yuan/ton compared to the average monthly theoretical profit of 3 yuan/ton in November. Driven by the pressure of losses, even with a weak trend in the price of the core raw material octanol, DOTP companies are still bucking the trend and raising prices to alleviate operational pressure.

The core ingredient, octanol, surged and then fell back.

Since November, affected by a combination of factors including worsening industry losses, companies proactively reducing production to support prices , and concentrated plant maintenance, many octanol plants have entered a state of shutdown for maintenance or reduced load operation. The octanol spot market supply quickly shifted from loose to tight, laying the foundation for price fluctuations. In early December, the tight supply situation for octanol further escalated. Previously reduced-production octanol plants failed to resume normal production as scheduled, and the market supply gap has not yet been filled. Coupled with maintenance plans for two new plants by two companies, the overall operating load of domestic octanol plants continued to decline, and the pressure of supply contraction intensified. Against this backdrop, the price increase of octanol in early December was significantly larger, and the increase was far higher than that of downstream DOTP products.

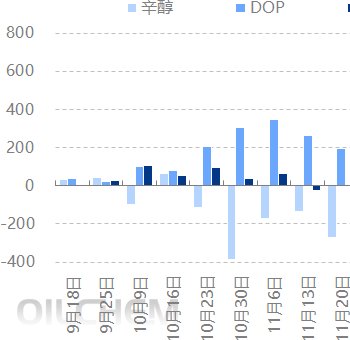

Comparison of average weekly profits in the DOTP industry chain in 2025 (RMB/ton) Figure 4. Theoretical Profit Trend of DOTP Enterprises (RMB/ton)

Data source: Longzhong Information

Since December, the DOTP industry has been mired in losses, failing to escape this predicament for most of the time. Taking the Zhejiang market as an example, as of now, the average monthly theoretical profit of sample companies has fallen to -119 yuan/ton, a significant decrease of 124 yuan/ton compared to the slight profit of 3 yuan/ton in November, highlighting the operational pressure on enterprises. At the beginning of this week, forced by continuous losses, DOTP companies proactively raised prices against the trend, significantly narrowing the theoretical loss margin. As of today, the theoretical profit of sample companies in Zhejiang has recovered to -30 yuan/ton, a significant improvement from -161 yuan/ton last Thursday . However,

demand has failed to provide effective support, with buyers continuing their cautious strategy of "buying on dips and waiting to see if prices rise," resulting in a lack of sustained momentum in market transactions. This directly restricts the upward movement of DOTP prices, leading to a slow pace of profit recovery for enterprises. Currently, the market is in a stalemate between supply and demand, and future trends will depend on changes in costs and demand.

Profitability recovery is uncertain; cost price trends are key.

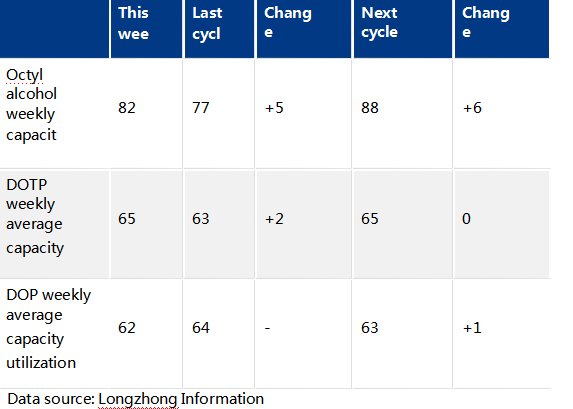

of DOTP Industry Chain Related Products and Forecast for Next Week

On the cost side, the supply and demand dynamics of the octanol market are a key factor influencing the DOTP market trend: Currently, domestic octanol social inventory is at a low level, with both factory and downstream user inventories remaining low.

From the supply side, octanol operating rates are expected to increase by 6% next week, and new plants are expected to come online later this month. Although the initial load increase may be relatively slow, its contribution to the increase in domestic octanol supply will be limited, with a small impact on the market in the short term. However, octanol production is expected to climb to a high level in January, significantly increasing supply pressure and leading to a lack of confidence among industry players regarding the future market. Considering the support from low short-term inventory and the expectation that domestic supply growth is likely to exceed demand growth,

the core raw material octanol market may slowly decline, negatively impacting DOTP market prices.

Figure 5. Changes in the DOTP main market price over the next three weeks (RMB/ton)

Data source: Longzhong Information

From the supply side, DOTP plant operating rates are expected to steadily increase, and spot supply in most parts of China will gradually become abundant, potentially putting pressure on some companies to accumulate inventory. Against this backdrop, most DOTP producers are expected to maintain an active order-taking strategy, focusing on flexible sales and accelerating inventory turnover through dynamic price adjustments.

The continued strengthening of expectations for ample supply in the overall market will exert downward pressure on DOTP prices.

Demand remained stable, with no substantial bright spots to support it. Downstream enterprises continued their purchases based on immediate needs and lower demand, showing little acceptance of current high-priced DOTP and weak purchasing enthusiasm. Affected by weak demand, the atmosphere for new orders in the DOTP market continued to decline, and some enterprises are already facing pressure from sluggish sales. In the short term, demand is unlikely to provide effective support to the market, and high-priced DOTP is beginning to come under pressure.

In summary, the current DOTP market is dominated by negative factors, with high- priced goods under significant pressure. However, the cost pressure on enterprises has not yet fully eased, which will effectively constrain the room for price concessions. It is expected that DOTP market prices may weaken in the short term, with the price fluctuation range in East China expected to be 7000-7400 yuan/ton in the latter half of the month. Whether the industry can achieve profitability in the future will depend heavily on the progress of new octanol production facilities and the pace of price

declines.