Introduction: The domestic 2-EH(Isooctyl Alcohol ) market began a downward trend this week, but due to low industry inventory levels, some factories slowly followed suit with price reductions, resulting in a stagnant market after the initial drop at the beginning of the week. Compared to the rapid rise in the 2-EH(Isooctyl Alcohol ) market earlier this week, the decline was relatively moderate.

I. Octyl alcohol market prices face downward pressure

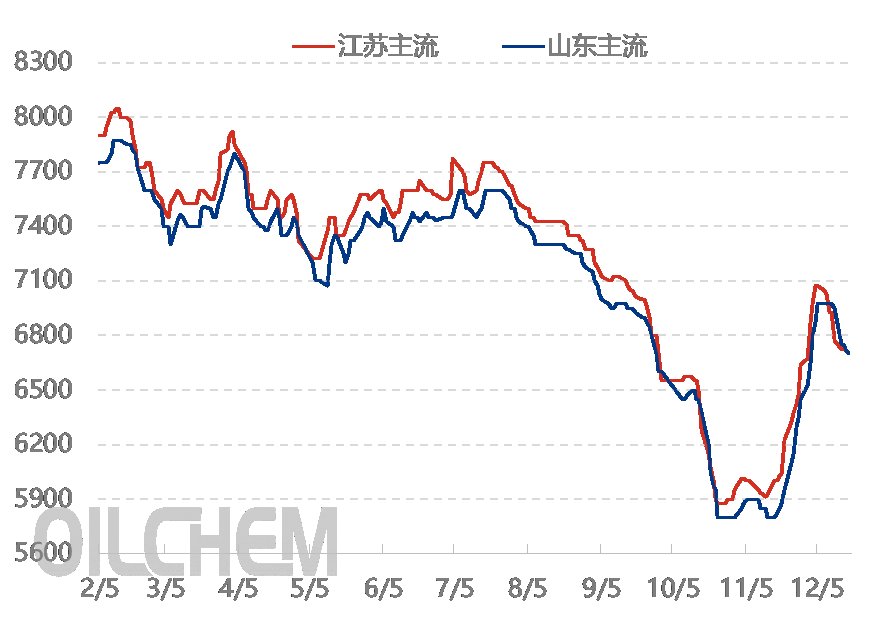

Figure 1. Price trend of 2-EH(Isooctyl Alcohol ) in the domestic market (RMB/ton)

After a rapid surge to high levels in early December, the price of 2-EH(Isooctyl Alcohol ) in the market failed to transmit the high prices effectively, leading to downward pressure on the market this week. As of Thursday, the ex-factory price in Shandong had fallen to 6,700 yuan/ton, a decrease of 250 yuan/ton from last week's high. The market decline was mainly due to anticipated increased supply, prompting traders to actively lower prices to move inventory, dragging down previous high-priced offers. This week, the operating rate of 2-EH(Isooctyl Alcohol ) plants increased compared to last week, with some factories experiencing significant pressure on spot sales. Most manufacturers maintained low inventory levels, supported by stable deliveries from contract customers. Downstream plasticizer prices had already fallen sharply last week, resulting in a cost inversion for

downstream users. This week, spot buying activity was weak, with an increased wait- and-see attitude. After lowering prices at the beginning of the week, manufacturers have once again entered a period of consolidation at low levels.

Increased industry operating rates and active sales by merchants

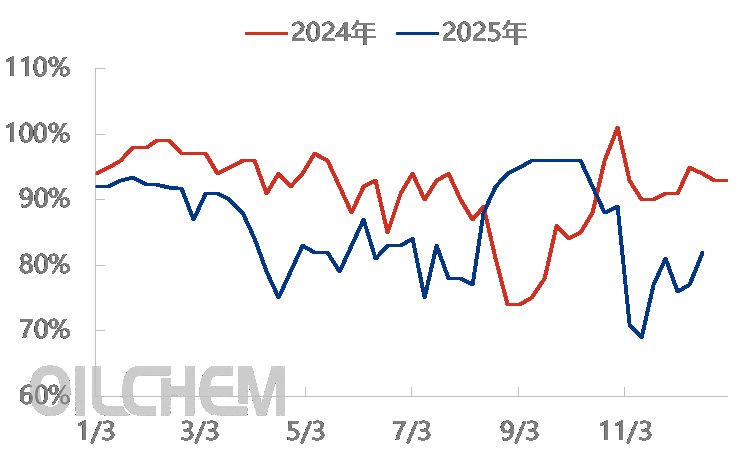

Figure 2. Weekly operating rate trend of 2-EH(Isooctyl Alcohol )

Data source: Longzhong Information

Two new 2-EH(Isooctyl Alcohol ) plants in Shandong and Jiangsu provinces started trial operations this week, but no output has yet been recorded. 2-EH(Isooctyl Alcohol ) plants that had previously undergone maintenance or reduced production have resumed operations this week, with the industry operating rate gradually recovering to around 82%, an increase of 5 percentage points from last week. Downstream plasticizer product operating rates remained generally stable, with DOP and DOTP industry operating rates fluctuating between 62-65%, resulting in stable 2-EH(Isooctyl Alcohol ) consumption. The 2-EH(Isooctyl Alcohol ) market has shifted from a supply shortage last week to a tight supply-demand balance.

This week, the market sentiment was generally bearish due to increased 2-EH(Isooctyl Alcohol ) supply. Traders maintained low inventory levels to mitigate the risk of a significant market downturn later. Merchants actively sold off their stock, and negotiated prices for actual transactions were slightly lower, putting downward pressure on high-end offers from factories.

I. Downstream products face significant spot cost pressures.

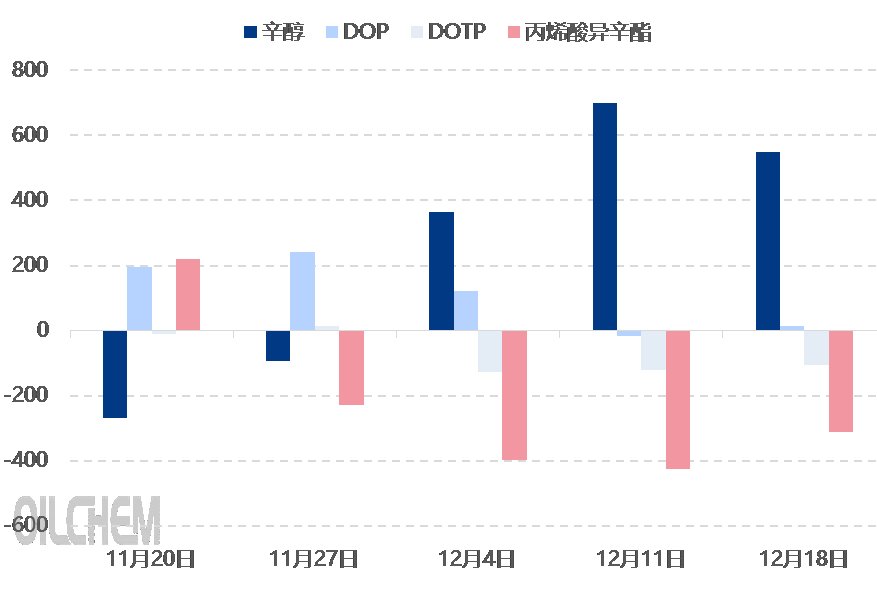

Figure 3. Profitability Comparison of Octyl Alcohol and Major Downstream Products (RMB/ton)

From the perspective of industry chain profitability, although 2-EH(Isooctyl Alcohol ) profits declined this week, it remains the most profitable sector within the industry chain, having held the top position for three consecutive weeks. Downstream DOP prices are near the cost line, resulting in a slight profit this week. Another major downstream product, DOTP, experienced a cost inversion in the spot market, but the spot losses eased somewhat this week, leading to increased capacity utilization at its plants. The cost inversion for iso2-EH(Isooctyl Alcohol ) acrylic acid remains severe, and some shut-down plants in East China have not yet restarted. Under pressure from high spot costs, core downstream users temporarily suspended spot 2-EH(Isooctyl Alcohol ) purchases this week, primarily fulfilling raw material contracts.

I. Shift in market supply and demand expectations leads to a downward trend in the market center of gravity.

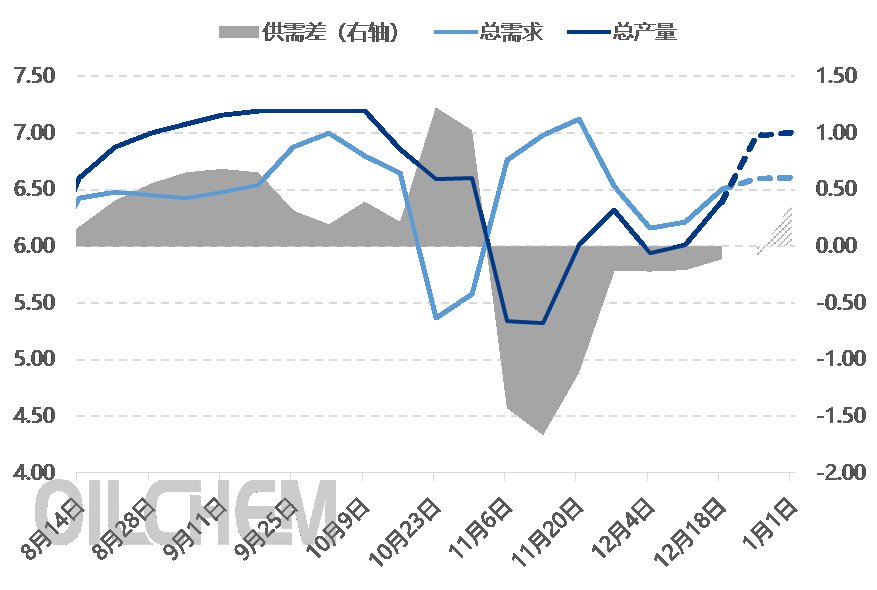

Figure 4. Supply and Demand Trend Forecast for Octyl Alcohol (10,000 tons)

As of mid-to-late December, domestic 2-EH(Isooctyl Alcohol ) social inventory remained at a low level. Due to the anticipated continued increase in 2-EH(Isooctyl Alcohol ) market supply, both factory and downstream user 2-EH(Isooctyl Alcohol ) inventories remained low. Looking at 2-EH(Isooctyl Alcohol ) plant operations, new plants are expected to start production in the latter half of this month, with operating rates gradually increasing. Therefore, the increase in domestic 2-EH(Isooctyl Alcohol ) supply from these new plants will be limited, and the impact on the market will be relatively small. 2-EH(Isooctyl Alcohol ) production is expected to rise to a high level in January, significantly increasing supply pressure.

From the demand side, downstream demand is expected to increase slowly, but the increase in demand will be less than the increase in 2-EH(Isooctyl Alcohol ) supply. Therefore, since late December, the supply-demand balance in the 2-EH(Isooctyl Alcohol ) market has reversed, with supply exceeding demand. The slow accumulation of industry inventory will continue to put pressure on the 2-EH(Isooctyl Alcohol ) market. Given the current low inventory levels and the fact that domestic supply growth exceeds demand growth, the 2-EH(Isooctyl Alcohol ) market is expected to gradually decline in the short term.