Published: 2025-08-22 17:03

Introduction: In August, the domestic C5 unit was affected by the temporary shutdown plan of some units, and the operating rate showed an overall downward trend, while the absolute value of demand reduction was even higher, and the market still had an imbalance between supply and demand.

1. Maintenance and restart intertwined with obvious periodic fluctuations

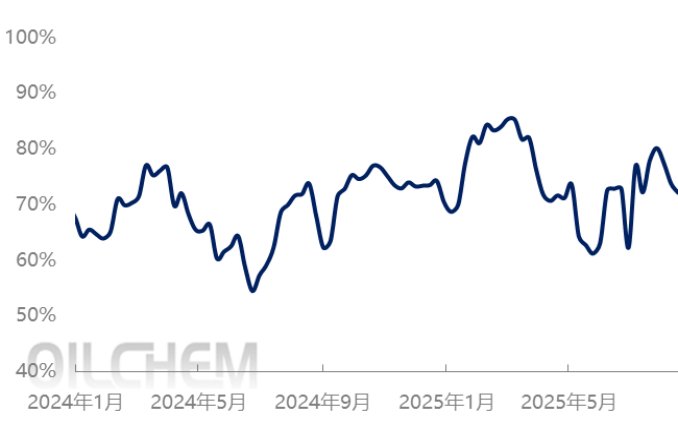

Figure 1 Statistics on weekly operating rates of China's C5 petroleum resins from 2024 to 2025

Entering August, the domestic C5 petroleum resin plant was affected by the temporary shutdown plan of some plants, and the operating rate showed an overall downward trend. As of August 22, the domestic C5 petroleum resin operating rate dropped from 80.08% on July 30 to this week. The C5 petroleum resin output was only 9,300 tons, and the operating rate was 72.06%, a decrease of 8.02 percentage points from the beginning of the month. In addition, in the short term, with the Puyang Bande Road, Fushun Huaxing, Xinjiang Tianli and other plants entering maintenance in early September, the plant operating rate is expected to continue to decline.

Table 1 C5 petroleum resin plant dynamics

Manufacturer Name | production capacity | Maintenance start time | Maintenance end time | Remark |

Fuhua Luhua | 3.6 | June 25 | August 25 | Routine maintenance |

Lanzhou Yahua | 2 | July 28 | August 25 | Device modification |

Puyang Ruisen | 2 | August 10 | September 10 | Temporary maintenance |

2. Demand is weak

Table 2 C5 petroleum resin supply and demand statistics

Unit: 1,000 tons

Data Type | data | This issue | Previous issue | Rise and Fall Value | Next Trend |

C5 petroleum resin for road marking paint | Yield | 5.34 | 5.54 | -0.2 | ↓ |

in stock | 14.6 | 14.1 | 0.5 | ↑ |

consumption | 4.8 | 5 | -0.2 | ↓ |

Adhesive C5 petroleum resin | Yield | 4.1 | 4.1 | 0 | → |

in stock | 23.1 | 22.1 | 1 | ↑ |

Total demand | 3.1 | 3.6 | -0.5 | ↓ |

Entering August, in the domestic C5 petroleum resin downstream hot-melt coatings, on the one hand, the previous inventory was digested, and on the other hand, the terminal start-up was still restricted by funds in various places, and the paint manufacturers' collection of payments was unfavorable. The usage was lower than expected. Under multiple negative factors, the manufacturers' procurement volume remained at a low level; in terms of hot-melt pressure-sensitive adhesives, the usage of hydrogenated petroleum resins further expanded, and the price difference with the adhesive C5 petroleum resin was still 1,400 yuan/ton. The more serious internal circulation in the label adhesive exacerbated the manufacturers' cautious purchasing mentality, the market transaction volume was insufficient, the oversupply intensified, and the price fell.

On the whole, some domestic C5 petroleum resin plants continued to undergo maintenance in early September, and the prices of adhesive C5 petroleum resin have gradually reached the psychological price of downstream recipients, and the supply of hydrogenated petroleum resin may be slightly tight due to increased demand. There is an expectation of an increase in market transaction volume, but in the short term, on-site inventory still needs to be digested, and the market may first enter the destocking stage. The prices of C5 petroleum resin have gradually stabilized at the bottom, or the repeated bottoming stage has ended, which also reflects the rhythm switch of the supply and demand relationship from adaptation to rebalancing.