Introduction: In the second quarter, the average market price of DBP in Henan Province was 7,566 yuan/ton, down 4.26% from the previous month and 16.06% from the previous year. In the second quarter, domestic DBP production increased by 0.4% from the previous month and decreased by 2.33% from the previous year. The average profit in Shandong Province increased by 59.59% from the previous month and increased by 25.2% from the previous year.

The DBP market fluctuated downward and fell to near the cost line

In the second quarter, the average market price of DBP in Henan Province was 7,566 yuan/ton, down 4.26% from the previous month and 16.06% from the previous year. The market price low was 7,400 yuan/ton and the price high was 7,900 yuan/ton, with an amplitude of 6.37%.

Figure 1 Domestic DBP Price Trend Chart from 2024 to 2025 (Yuan/ton)

Data source:

In the second quarter, the domestic DBP market price continued to fall. First, on the raw material side, both n-butanol and naphthalene phthalic anhydride maintained a volatile downward trend in the second quarter, so that the cost of DBP continued to decline. Although the cost pressure was relieved, the support for its price continued to weaken; secondly, there was no sign of improvement in the overall downstream demand. In the early second quarter, it was affected by the tariff policy, which led to the restriction of terminal product exports. Although the policy was relaxed in the later period, the downstream basically entered the off-season, resulting in a heavy bearish sentiment among market participants. The overall market inquiries and transactions were sluggish. Although the production plants were shut down for maintenance one after another, the inventory level remained high due to the obstruction of factory shipments. The market supply was sufficient, and the oversupply situation continued to accelerate. In addition, the raw material prices continued to fall, so the production plants also continued to make concessions for shipments. Near the end of the quarter, the DBP price fell to near the cost line, once again setting a new low for the whole year.

2. The decline in both raw materials drives down DBP prices

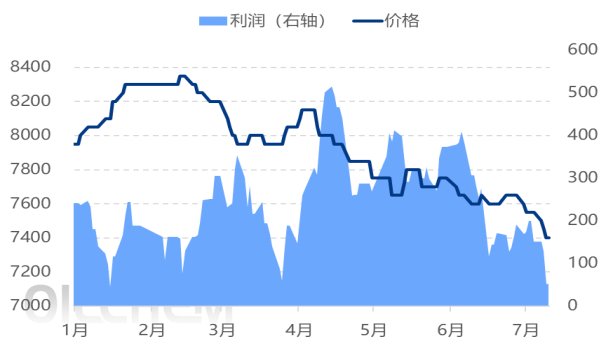

The main factors for the decline in DBP market prices in the second quarter include the decline in both raw materials, naphthalene-based phthalic anhydride and n-butanol, which weakened the cost support. According to statistics, the cost of DBP in Shandong market in the second quarter decreased by 5.97% month-on-month and 17.44% year-on-year. As both raw materials declined, the cost decreased significantly, while the decline in DBP prices was smaller than the cost. Therefore, the average profit in the second quarter was 308 yuan/ton, an increase of 59.59% month-on-month and 25.2% year-on-year.

Figure 2 Comparison of domestic DBP prices and profits in 2024-2025 (yuan/ton)

Data source:

In the second quarter, naphthalene-based phthalic anhydride (NPA) was heavily impacted by industrial naphthalene, resulting in a volatile and weak market. This was the smallest decline within the industry chain during the quarter, with the average price of NPA at 6,542 yuan/ton, a 2.97% decrease from the first quarter and an 11.77% decrease from the same period last year. Meanwhile, the market for n-butanol, another NPA, showed a significant downward trend. It is reported that the domestic market has seen increased bearish sentiment due to the commissioning of new plants in the second quarter. Coupled with the downstream market entering its off-season, overall demand has been bleak, hindering factory shipments. However, manufacturers have been forced to maintain low inventory levels, resulting in continuous discounts. The average price in the second quarter was 6,282 yuan/ton, a 9.62% decrease from the first quarter and a 23.87% decrease from the same period last year, marking the largest decline in the industry.

product | area | 2025Q2 | 2025Q1 | 2024Q2 | Month-on-month | Year-on-year |

DBP | Henan region | 7566 | 7903 | 9014 | -4.26% | -16.06% |

n-Butanol | Shandong region | 6282 | 6951 | 8252 | -9.62% | -23.87% |

Naphthalene-based phthalic anhydride | Hebei region | 6542 | 6742 | 7415 | -2.97% | -11.77% |

DBP Cost | Shandong region | 7468 | 7942 | 9046 | -5.97% | -17.44% |

DBP Profit | Shandong region | 308 | 193 | 246 | 59.59% | 25.20% |

Data source: |

3. Costs are reduced while profits remain high. DBP supply is relatively stable.

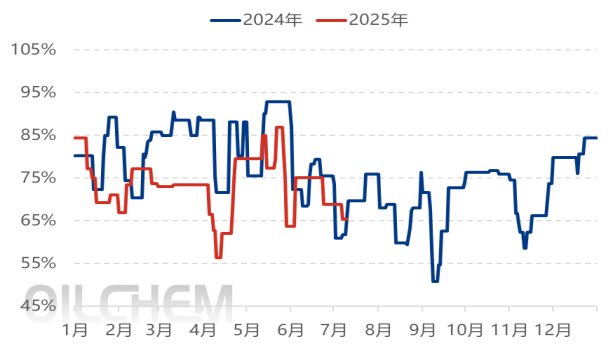

Figure 3: Domestic DBP Capacity Utilization Trends from 2024 to 2025

Data source:

While DBP market prices fluctuated and weakened during the quarter, DBP profits showed an upward trend, as the decline in market prices was smaller than the decline in costs. Consequently, despite the bleak downstream market, DBP production and output remained relatively stable, with minimal fluctuations. DBP production in the second quarter reached 175,800 tons, a slight increase of 0.4% from the first quarter and a year-on-year decrease of 2.33%. DBP capacity utilization was 73.45% in the second quarter, down 0.8 percentage points from the first quarter, primarily due to the shorter production days in February. Production peaked in May, at approximately 66,800 tons, and was lowest in April, at approximately 54,100 tons.

Data Type | 2025Q2 | 2025Q1 | 2024Q2 | Month-on-month | Year-on-year |

Yield | 17.58 | 17.51 | 18 | 0.40% | -2.33% |

Capacity Utilization | 73.45% | 74.25% | 77.82% | ↓0.8 percentage points | ↓4.37 percentage points |

Data source: |

IV. Market Forecast

From the perspective of the raw material market, new production capacity will be put into production in the raw material n-butanol market in the third quarter, and at the same time, the maintenance equipment will resume production one after another. The overall supply is showing an increasing trend. The downstream of n-butanol will still be in the off-season, and it is expected to enter the peak season at the end of the third quarter. However, in the face of the increase in n-butanol production, market participants and downstream companies keep raw material inventories at a low level and purchase on demand. It is expected that the n-butanol market will continue to maintain a volatile downward trend in the third quarter.

From the demand side, July and August in the third quarter are the hottest periods, which is the off-season for consumption in the terminal downstream market. Therefore, the market demand will gradually weaken further.

From the supply side, DBP's equipment was shut down for a long time for maintenance in the third quarter, and there is room for production to decline, but the factory's inventory level continues to be medium to high, so the market supply is sufficient.

In summary, it is expected that both domestic DBP supply and demand will show a downward trend in the third quarter, and the oversupply in the market will continue. At the same time, the new production capacity of raw material n-butanol will further lower the raw material price after it is put into production. At that time, the DBP cost will follow suit and further weaken the support for DBP price, resulting in fewer positive factors in the DBP market. For this reason, market participants will mainly purchase on dips based on just-in-time needs. It is expected that the DBP market price will fluctuate and run weakly in the third quarter, and there is an expectation of further refreshing low prices.