Published: 2025-08-09 11:57 Source: Longzhong Information Editor : Liu Wenluan

Introduction: Since late July, the domestic octanol market has been declining, and the market has been under pressure from both supply and demand. Industry players lack confidence in the future trend, and octanol factories and downstream users have maintained low inventory operations.

1. Octanol market center of gravity continues to decline

Octanol market weekly average price statistics (yuan/ton)

area | July 18 | July 25 | August 1 | August 8 |

Shandong | 7515 | 7600 | 7485 | 7365 |

Jiangsu | 7655 | 7730 | 7615 | 7485 |

Domestic octanol prices have fallen again to a two-month low. Spot prices in Shandong Province reached 7,300 yuan/ton ex-factory on Friday. Buyers maintained a moderate pace of purchasing raw materials, resulting in a lukewarm market. In August, octanol supply showed an upward recovery trend. Anticipating increased supply, manufacturers and intermediaries actively shipped goods at the beginning of the month, leaving the market's core focus lacking supply support. Low transaction prices for some forward deliveries have impacted market confidence, putting pressure on the core focus. Downstream plasticizer and 2-ethylhexyl acrylate products face significant cost pressures, particularly for 2-ethylhexyl acrylate, resulting in low industry operating rates and declining demand for octanol. Consequently, under pressure from supply and demand fundamentals, the octanol market has experienced a downward trend over the past two weeks.

II. Analysis of regional supply changes in the octanol market

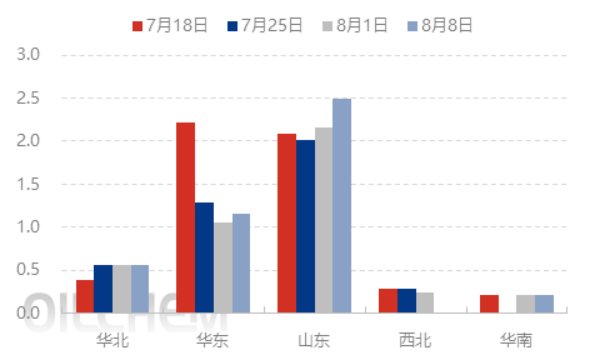

Figure 1 Weekly output changes in major domestic octanol production areas (10,000 tons)

Data source: Longzhong Information

Looking at domestic octanol production changes over the past four weeks, the two regions with the largest production changes are East China and Shandong. East China's octanol production fell 48% from mid-September, primarily due to significant supply losses caused by the shutdown and maintenance of the Anqing Shuguang Phase II plant. This week, the Zhejiang Satellite octanol plant increased its capacity, leading to an increase in East China octanol production compared to last week. With the restart of the Anqing Shuguang Phase II plant over the weekend, octanol supply in East China will return to normal, easing tight spot supply in the region. Shandong's octanol supply has gradually recovered over the past two weeks, with the restart of the Qilu Petrochemical plant increasing supply in the region. Due to the high operating capacity of local octanol plants, local octanol companies are actively shipping, and product orders remain in pre-sale status.

Currently, a unit in Northwest China is shut down for maintenance and is expected to resume operations in mid-to-late August. New octanol units in Northwest China are ramping up slowly, significantly impacting market supply. Following maintenance in July, octanol supply in North and South China has remained stable.

3. Downstream cost inversion affects its enthusiasm for starting production

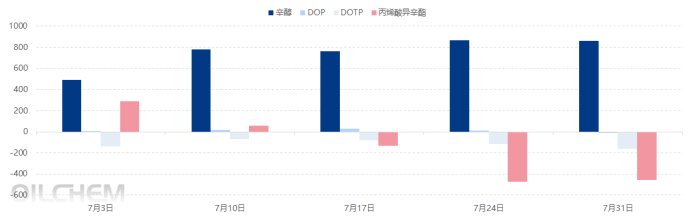

Figure 2 Comparison of domestic octanol and main profits (yuan/ton)

Data source: Longzhong Information

Looking at the profitability of octanol and its major downstream products, octanol has the greatest potential for profit, while downstream products are all experiencing price inversion, with 2-ethylhexyl acrylate experiencing significant losses. As of August 8, octanol's profit in Shandong Province was 620 yuan/ton. Due to the gradual decline in octanol prices, the losses of downstream plasticizers have slightly improved. On Friday, DOP product prices fluctuated around cost, with some regions experiencing small profits. DOTP and 2-ethylhexyl acrylate continue to experience price inversion.

Figure 3 Trends in the operating rates of domestic octanol and major downstream industries

Data source: Longzhong Information

Due to recent maintenance at domestic octanol plants, octanol capacity utilization has fallen to 80%. Operating rates for key downstream products, such as DOP and DOTP, have rebounded, and plasticizer plant operations have increased to above medium capacity, increasing rigid demand for octanol products. However, based on spot octanol prices, plasticizer products are operating near cost. With octanol prices falling to a two-month low on Friday, spot plasticizer cost pressures have eased somewhat. The cost of isooctyl acrylate products is significantly inverted, and operating rates have recently declined, reducing octanol consumption.

4. Octanol market continues to be weak

After mid-August, domestic octanol supply continued to recover, easing tight spot market conditions. Meanwhile, the downstream plasticizer market saw lukewarm trading, primarily driven by periodic restocking at low prices. Downstream users also maintained a low-price purchasing strategy for octanol raw material. With no significant improvement in supply and demand, the octanol market lacked confidence, and aggressive selling by industry players will continue to weigh on the market. The octanol market is expected to remain weak in the second half of the month. Given the slow pace of new capacity coming online, the market's potential for decline is limited.