As a mainstream environmentally friendly plasticizer, DOTP's market trends are closely linked to upstream and downstream supply chains. The third quarter, traditionally the industry's transition window from off-season to peak season, has historically exhibited distinct cyclical characteristics. By reviewing historical third-quarter DOTP market data, we can understand its price fluctuation patterns, driving factors, and potential future trends.

1. Historically, the supply and demand of the DOTP market were both low in the third quarter.

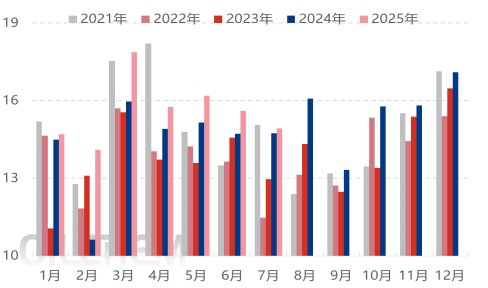

Figure 1 Comparison of DOTP monthly production from 2021 to 2025 (10,000 tons) Figure 2 DOTP quarterly apparent consumption trends from 2021 to 2025 (10,000 tons)

From the four-year cycle from 2021 to 2025, the monthly production data of DOTP shows significant seasonal characteristics: the production from July to September is at the 8th to 10th level of the year in most years, and is generally in the medium to low range of the year.

The demand side also has distinct seasonal patterns: historical data shows that the apparent demand for DOTP in the third quarter is at its lowest point of the year every year; and July and August are the traditional off-seasons for downstream demand in the DOTP market, and the weak demand trend is more prominent. The core influencing factors mainly include two aspects: 1. Direct constraints of climate on the production side: High temperatures will not only affect the downstream construction progress and product production efficiency, but will also cause the operating rate of the downstream DOTP industry to decline to varying degrees; 2. Seasonal adjustments to product formulas: Taking the film industry as an example, in hot weather, the proportion of plasticizers added in the product production process will be proactively reduced, further weakening the market's purchasing demand for DOTP.

Due to the dual influence of weak demand and inventory levels, the enthusiasm of DOTP manufacturers to start production has been significantly suppressed. Therefore, the overall operating rate of the industry in July and August is usually at a lower-middle level during the year.

However, based on currently known production dynamics of DOTP companies (including shutdown and reduction plans), DOTP production is projected to be around 165,000 tons in August 2025, a modest increase from July. Coupled with the fact that most DOTP manufacturers have already accumulated significant inventory, the pressure of oversupply in the market is expected to intensify.

2. Historically, the DOTP market has been primarily loss-making in the third quarter.

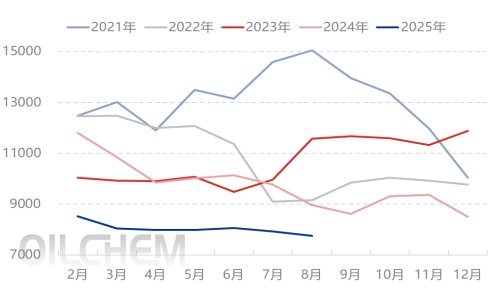

Figure 3 DOTP monthly profit comparison chart from 2021 to 2025 (yuan/ton)

The pressure of oversupply in the market continues to be transmitted to the profit side, directly leading to the continuous compression of the theoretical profit margins of DOTP companies. Judging from the average monthly profit data of DOTP from 2021 to 2025, July and August have become the "trough" period for industry profits. During this period, the average monthly profit of companies is in the red in most years, and seasonal profit pressure is significant.

However, the industry's profit structure has seen positive changes on the cost side: starting in the second half of 2024, the expansion of octanol production capacity has significantly accelerated. Increased market supply has driven a steady decline in octanol prices, gradually easing the raw material cost pressures faced by DOTP companies. This positive factor has directly led to improved industry profitability. Since 2025, DOTP companies have achieved theoretical profitability for most of the time, breaking the previous profit dilemma.

However, the good times didn't last long. After July 2025, the industry's profitability reversed again, with DOTP companies shifting from profitability back into the red. This loss pattern shows no signs of improvement. For example, DOTP companies in Zhejiang Province still see theoretical losses of 81 yuan per ton as of the latest data, reflecting the current profitability pressures facing the industry.

3. Historically, DOTP prices have tended to rise from low levels in the third quarter.

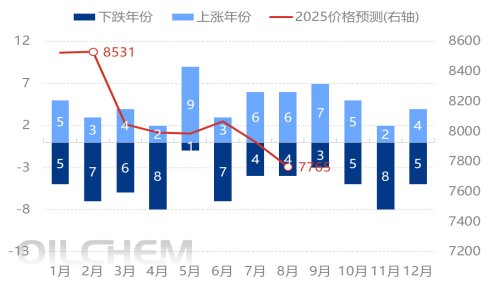

Figure 4 Comparison of DOTP monthly average price trends from 2021 to 2025 (yuan/ton) Figure 5: China's DOTP monthly price fluctuations from 2015 to 2024 and price trends in 2025 (yuan/ton)

Judging from the average monthly price data of DOTP in the ten years from 2015 to 2024, although July to September are in a relatively low range of the year, the price trend shows the characteristics of "more increases than decreases", and in most years a seasonal pattern of "bottoming out in June and gradually rising thereafter" will be formed.

A deeper analysis of the price fluctuation logic reveals that there are significant differences in the market drivers in different directions:

In years of rising prices, market activity often relies on the support of the raw material octanol. When the octanol market experiences supply shortages and price increases, the cost side of the equation drives DOTP prices higher. However, it's worth noting that these price increases often struggle to be effectively transmitted to profits. Due to limited downstream acceptance of higher prices, cost pressures are not smoothly transferred downward. Even with DOTP price increases, companies generally remain in a theoretical loss-making position, making poor cost transmission a key pain point.

In the price-falling cycle, the market is more affected by the combined negative impact of "raw material costs + downstream demand": on the one hand, if the price of octanol weakens, the cost support of DOTP will also decline simultaneously; on the other hand, the downstream demand in the third quarter lacked favorable support for most of the time, coupled with the long-term oversupply pressure in the market, these two factors jointly dragged down the DOTP price to show a weak trend.

IV. New Characteristics of Factors Influencing the Current DOTP Market: Raw Material Capacity Expansion Expectations Become a Key Variable

Based on historical performance, the DOTP market's third-quarter trends were primarily driven by three key factors. First, demand showed a transition from off-season to peak season. July and August were traditionally off-season for the downstream PVC products industry, with weak orders suppressing DOTP demand. While demand theoretically entered a period of improvement in September, providing some support for market prices and corporate profits, a weak peak season has become the norm in recent years, and the strength of the demand recovery will directly determine the extent and sustainability of the September rebound. Second, overcapacity in DOTP has long constrained upward momentum. Since 2022, the DOTP industry's capacity utilization rate has remained between 50% and 60%. This oversupply has severely limited price growth, even in the face of cost-driven growth or a slight increase in demand, making a sustained upward trend difficult. Third, changes in the cost side have become a key variable that distinguishes this year from previous years. Currently, the expected capacity expansion of raw material octanol has continued to have a negative impact on the upstream and downstream mentality of the DOTP market: upstream companies are worried that the oversupply of octanol after the capacity expansion will put pressure on prices, while downstream companies are skeptical about the stability of cost transmission. This general cautious mentality has further spread, and ultimately formed a clear bearish drag on DOTP prices, breaking the traditional pattern of occasional cost support for prices in the third quarter of previous years, and becoming a special cost factor that the market needs to pay attention to this year.

Table: Statistics of Octanol Planned New Capacity in the Second Half of 2025 (Unit: 10,000 tons/year)

area | Company Name | Craftsmanship | production capacity | Production time |

northwest | Ningxia Jiuhong | Oxo synthesis | 14 | It has been put into production in July 2025 |

Shandong | Shandong Jianlan | Oxo synthesis | twenty one | September-October 2025 |

East China | Jiangsu Huachang | Oxo synthesis | 14 | Fourth quarter of 2025 |

South China | BASF (Zhanjiang) | Oxo synthesis | 15 | Fourth quarter of 2025 |

Total new production capacity in 2025 |

| 64 |

|

According to Longzhong Information, the octanol market is expected to see approximately 640,000 tons of new production capacity added in the second half of 2025. With the exception of Ningxia Jiuhong, which has already successfully commenced production, the remaining three companies plan to release new capacity in the fourth quarter. This means that in the short term, the impact of new capacity on the actual supply of octanol will be relatively limited, with its impact primarily reflected in disrupting market sentiment.

Judging from current market fundamentals, raw material octanol manufacturers generally maintain low inventory levels. This situation will continue to limit the potential for price concessions in the short term, thereby providing a low-price support for the DOTP market and preventing a significant price decline. However, from a long-term perspective, given the clear expectation of new production capacity release, market participants are generally cautiously bearish. As a result, the DOTP market may struggle to escape a volatile and weak market.